Every business, whether it is a small café or a multinational corporation, needs money to operate. Money is required to purchase resources, pay employees, invest in equipment, market products, and expand operations. The management of money within a business is known as finance.

Finance refers to the planning, acquisition, management, and control of financial resources to achieve business objectives. In IB Business Management, finance plays a critical role because financial decisions affect every department of an organization. Production requires money to buy machinery, marketing needs funds for advertising, and human resources requires money to pay salaries.

A business that manages its finances effectively is more likely to survive, grow, and remain competitive. Poor financial management can lead to serious problems such as cash shortages, inability to pay debts, or even bankruptcy.

Finance allows businesses to:

For example, when a new restaurant opens, the owner must invest money to rent a building, buy kitchen equipment, hire staff, and advertise. Without proper financial planning, the restaurant may struggle to survive even if the food quality is excellent.

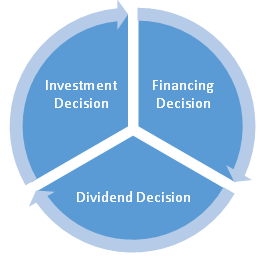

Key Financial Decisions

Managers usually make three major financial decisions:

These decisions shape the business's long-term success.

Businesses require finance at different stages of their life cycle. A start-up requires capital to begin operations, while an established firm may need funds for expansion or modernization. The different methods businesses use to obtain money are known as sources of finance.

Sources of finance can be broadly classified as internal or external.

Retained Profit: Portion of profit kept in the business rather than distributed to owners. Advantages: no interest payments, no loss of control. However, amount available may be limited.

Sale of Assets: Businesses may sell unused or outdated assets to raise funds.

Personal Savings: Entrepreneurs often use their personal savings to start a business.

Bank Loans: Money borrowed from a bank that must be repaid with interest. Advantages: large amounts, predictable repayment. Disadvantages: interest, collateral may be required.

Share Capital: Companies raise finance by selling shares to investors (ordinary shares or preference shares).

Venture Capital: Investment from specialized investors in exchange for equity.

Government Grants: Funds from government that do not require repayment but often have strict conditions.

Trade Credit: Allows businesses to receive goods from suppliers and pay later (typically 30–90 days).

Short-Term vs Long-Term Finance

Selecting the appropriate source of finance depends on factors such as cost, risk, flexibility, and control.

To evaluate financial performance, businesses must understand the relationship between costs and revenues.

Revenue refers to the income a business receives from selling goods or services.

Revenue = Price × Quantity Sold

For example, if a company sells 1,000 units of a product at $10 each, the total revenue will be $10,000. Businesses aim to maximize revenue by increasing sales volume, improving product value, or expanding into new markets.

Remain constant regardless of production level. Examples: rent, salaries, insurance. Even if production is zero, fixed costs must still be paid.

Change directly with production levels. Examples: raw materials, packaging, direct labour. If production increases, variable costs also increase.

Total Cost = Fixed Cost + Variable Cost

Average Cost = Total Cost ÷ Quantity Produced

Profit = Total Revenue − Total Costs

Gross Profit = Revenue − Cost of Goods Sold

Net Profit = Gross Profit − Operating Expenses

Understanding cost structures helps managers set prices, control expenses, and improve profitability. Profitability is essential for long-term business sustainability.

At the end of each financial year, businesses prepare financial statements to evaluate their financial performance. These statements are known as final accounts. Final accounts provide information to various stakeholders, including managers, investors, banks, and government authorities.

The income statement, also known as the profit and loss account, shows the financial performance of a business over a specific period. It records: revenue, cost of goods sold, gross profit, operating expenses, and net profit. The income statement helps managers determine whether the business is making a profit or a loss.

The balance sheet shows a business's financial position at a particular point in time. It consists of three major components:

The balance sheet follows the accounting equation: Assets = Liabilities + Equity. This equation must always balance.

Importance of Final Accounts

Final accounts help businesses assess financial performance, track profitability, plan future strategies, and provide information to investors. Without financial statements, it would be extremely difficult for managers to make informed decisions.

Financial ratios are tools used to analyze a company's financial health. They allow managers and investors to compare performance over time or with other businesses. Two major categories of ratios studied in IB Business Management are profitability ratios and liquidity ratios.

Gross Profit Margin = (Gross Profit ÷ Revenue) × 100

Indicates the percentage of revenue remaining after production costs. Higher margins indicate efficient production and pricing strategies.

Net Profit Margin = (Net Profit ÷ Revenue) × 100

Shows the business's overall profitability after all expenses. A rising net profit margin indicates improved financial performance.

Current Ratio = Current Assets ÷ Current Liabilities

A ratio above 1 usually indicates that the business can meet short-term debts.

Quick Ratio (Acid Test) = (Current Assets − Inventory) ÷ Current Liabilities

This ratio provides a stricter measure of liquidity by excluding inventory. Liquidity is important because even profitable businesses can fail if they run out of cash.

Businesses often use a combination of debt (borrowed money) and equity (owners' funds) to finance their activities. The balance between these two sources is extremely important because it affects the financial stability and risk level of the organization.

The debt-to-equity ratio measures the proportion of a company's financing that comes from borrowing compared with the amount invested by owners or shareholders.

Debt/Equity Ratio = Total Liabilities ÷ Shareholders' Equity

This ratio helps stakeholders understand how much financial risk a company is taking.

Interpreting the Ratio

A high debt-to-equity ratio indicates that a business relies heavily on borrowed funds. This can increase financial risk because the business must make regular interest payments regardless of whether profits are high or low.

A low debt-to-equity ratio indicates that a business relies more on shareholders' funds. This generally suggests lower financial risk but may limit growth if insufficient funds are available.

Example: If a manufacturing company has total liabilities = $500,000 and shareholder equity = $250,000, then Debt/Equity Ratio = 500,000 ÷ 250,000 = 2. This means the company uses twice as much debt as equity to finance its operations.

Advantages of Debt Financing: Owners maintain full control; interest payments are often tax-deductible; allows companies to grow quickly by accessing large funds.

Risks of High Debt Levels: Large interest payments; difficulty obtaining additional loans; increased financial risk during economic downturns.

Therefore, financial managers must carefully maintain a balanced financial structure.

Profit and cash are not the same thing. A business may be profitable but still face financial problems if it lacks sufficient cash to meet its obligations.

Cash flow refers to the movement of money into and out of a business over time.

Money entering the business: sales revenue, loans received, capital invested by owners, sale of assets.

Money leaving the business: wages and salaries, rent and utilities, purchase of raw materials, loan repayments, taxes.

A cash flow forecast is a financial planning tool that estimates future cash inflows and outflows over a specific period. It helps businesses anticipate potential cash shortages and plan accordingly.

Format: Opening Balance + Cash Inflows − Cash Outflows = Closing Balance

Example: Opening Balance = $10,000; Inflows = $5,000; Outflows = $7,000; Closing Balance = $8,000

Managers use this information to plan financing needs and adjust spending.

Methods to Improve Cash Flow

Efficient cash management strengthens financial stability. Poor cash flow management is one of the most common reasons why businesses fail, particularly during the early stages.

Businesses often face decisions about whether to invest in new projects, machinery, technology, or expansion. These decisions involve large financial commitments, so managers must evaluate whether the investment will generate sufficient returns. The process of evaluating potential investments is known as investment appraisal.

Measures how long it takes for an investment to recover its original cost.

Payback Period = Initial Investment ÷ Annual Cash Inflow

Example: A company invests $20,000 in new machinery generating $5,000 profit per year. Payback = 20,000 ÷ 5,000 = 4 years.

Advantages: Simple and easy to calculate, useful for businesses with limited cash. Limitations: Ignores profits after the payback period, does not consider the time value of money.

Measures the profitability of an investment relative to its cost.

ARR = (Average Annual Profit ÷ Initial Investment) × 100

Example: Initial investment = $50,000; Average annual profit = $10,000; ARR = (10,000 ÷ 50,000) × 100 = 20%

Advantages: Considers overall profitability, easy to compare different investments. Limitations: Does not consider the timing of cash flows.

NPV is a more advanced investment appraisal technique that considers the time value of money — money received today is worth more than money received in the future.

NPV = Present Value of Cash Inflows − Initial Investment

If NPV is positive, the investment is financially worthwhile. If NPV is negative, the investment should usually be rejected. Although NPV provides more accurate results, it is more complex to calculate.

A budget is a financial plan that outlines expected revenues and expenses over a specific period of time. Budgets help businesses allocate resources efficiently and control spending.

A variance occurs when actual financial results differ from the budgeted figures.

Managers analyze variances to identify problems and improve future planning.

Benefits of Budgeting

GreenBite is a small company that produces organic snack bars. The business started three years ago with funding from the founder's personal savings and a small bank loan.

Due to growing demand for healthy food products, the company is considering expanding production by purchasing new machinery worth $80,000.

The financial manager prepares the following information:

The company must decide whether the investment will improve long-term performance.

Case Study Reflection

Think about the financial concepts learned in this lesson and reflect on GreenBite's situation.

Understanding these financial tools allows managers to make informed decisions that support business growth.

Finance is one of the most essential functions of any business organization. From raising funds to evaluating investments and controlling expenses, financial management influences nearly every decision made within a company.

Throughout this lesson, several important financial concepts were introduced:

When these financial tools are used together, they allow businesses to make strategic decisions, manage risks, and achieve sustainable growth.

Finance is not only about numbers; it is about making informed choices that shape the future of an organization.